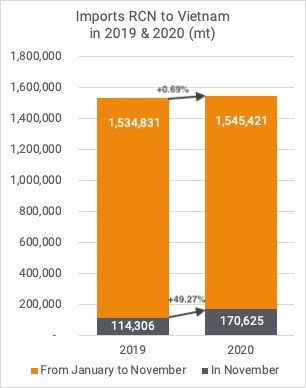

If we add all these numbers up, Vietnam’s own crop of about 400,000 mt RCN + 1,545,421 mt imported + the equivalent of 228,484 mt for the raw kernels with Testa, we get to a total of 2,173,905 mt which, with a kernel outturn of (on average) about 22%, makes about 478,259 mt of (exportable) kernels.

Export

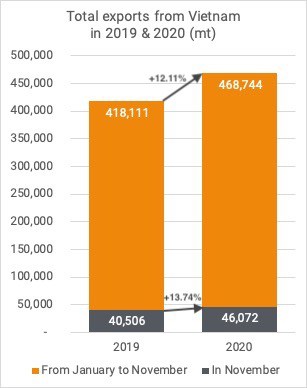

Vietnam exported 46,072 mt of cashew kernels in November 2020. It is 13.74% more in comparison to the same month in 2019. Since the beginning of the year, Vietnam exported 12.11% more than the period January-November last year. Despite the pandemic crisis, a total of 468,744 mt of cashew kernels were exported.

So, with an estimated total production of exportable kernels of 478,259 mt (of which 468,744 mt was actually exported), the difference is presumably being consumed domestically in Vietnam.

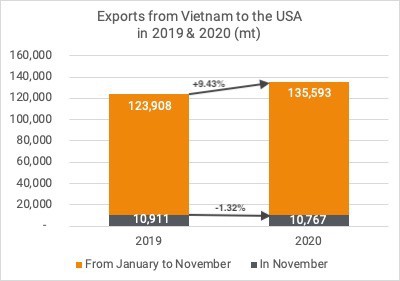

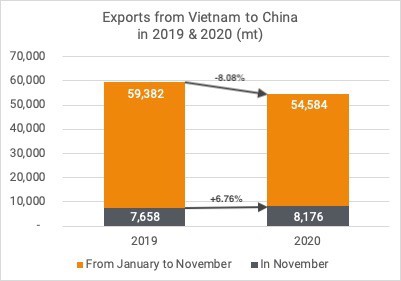

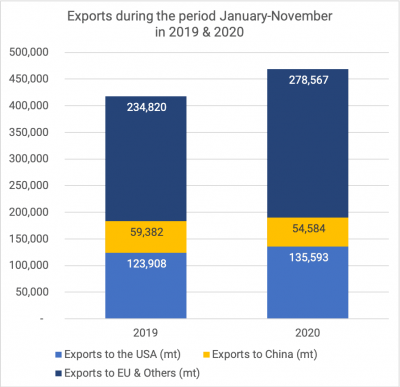

Demand is particularly high in the EU (+18.63% since the beginning of the year) and the US (+9.43% since January). However, demand from China decreased this year by about 8% compared to last year. This is a consequence of the Covid-19 crisis. During several months, the exports to China were extremely low, and the high shipments from the past months did not allow to reach the volume exported to China in 2019.

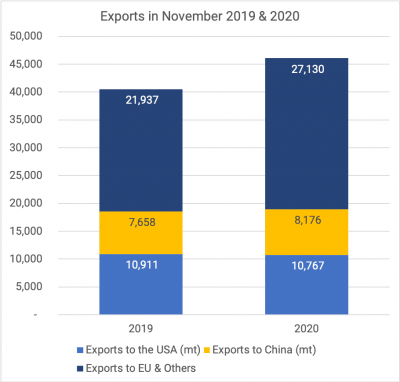

United States

To the USA, Vietnam shipped 10,767 mt in November, 1.32% less than last year.

During the period January-November 2020, the exports to the USA increased by 9.43% to 135,593 mt.

China

8,176 mt were exported to China in November, which is 6.76% more than last year. Exports to China are still increasing but the rate reduced, since the peaks in September and October. Since January 2020, 54,584 mt have been exported, and that is 8.08% less than last year.

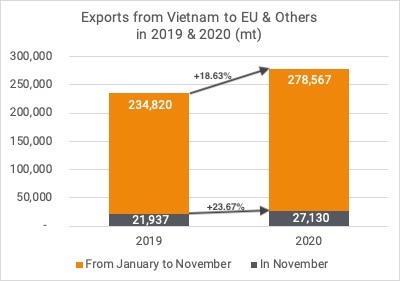

Europe

To the EU & others, Vietnam shipped 27,130 mt, which is 23.67% higher than November 2019. The total for the EU & others so far in 2020 is 278,567 mt, thus 18.63% higher than last year.

Just like in most of the past months, exports from Vietnam are higher than in 2019. RCN imports, which in previous months were lower, finally caught up and have now reached a similar level as in 2019. This extraordinary year, marked by the Covid-19 crisis, does not seem to have affected the processing, trade, nor consumption of cashews.

Market & production dynamics